RBI Cuts Rate to 5.25%: Cheaper Loans & GDP Boost (Dec 2025)

Good news for borrowers! RBI reduces repo rate to 5.25%. Read our full analysis on the "Goldilocks" economy and exactly how much you will save on your loans.

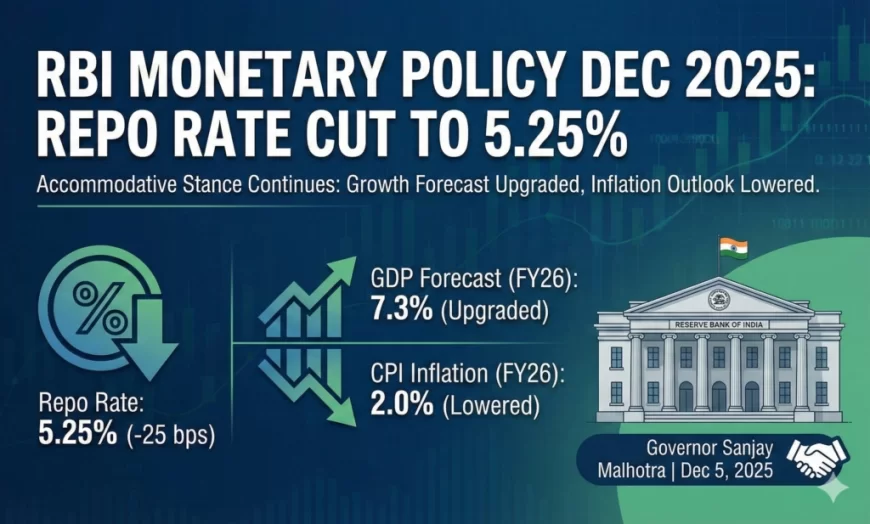

In a decisive move that underscores the robust health of the Indian economy, the Reserve Bank of India’s (RBI) Monetary Policy Committee (MPC) unanimously voted to cut the policy repo rate by 25 basis points (bps) to 5.25% on December 5, 2025. This decision, led by Governor Sanjay Malhotra, marks the fourth rate cut of the calendar year, bringing the cumulative reduction in 2025 to 125 bps.

Also Read: RBI Ready To Support Sectors

As reported by

This comprehensive analysis delves into the nuances of the December 2025 monetary policy, its immediate impact on your finances, and the broader economic implications for FY26.

The "Goldilocks" Economic Backdrop

The term "Goldilocks economy" refers to a state that is not too hot (causing inflation) and not too cold (causing a recession)—it is just right. The RBI’s decision was heavily influenced by data that paints exactly this picture for India.

-

Robust Growth: India’s real Gross Domestic Product (GDP) growth accelerated to an impressive 8.2% in the second quarter of FY26. This resilience, driven by strong domestic consumption and investment, has allowed the central bank to focus on supporting growth without fear of overheating the economy.

-

Benign Inflation: Perhaps the most critical factor was the dramatic fall in headline inflation. In Q2 FY26, average headline inflation dropped to 1.7%, breaching the RBI’s lower tolerance threshold of 2%. By October 2025, it had dipped further to a mere 0.3%.

Governor Malhotra highlighted that this unique combination of "inflation at a benign 2.2% and growth at 8% in H1:2025-26" provided the necessary policy space to support growth momentum further.

Key Policy Highlights: December 2025

Beyond the headline rate cut, the MPC meeting revealed several critical adjustments to India’s monetary framework:

-

Repo Rate: Reduced by 25 bps to 5.25%. This is the interest rate at which the RBI lends to commercial banks. A lower rate typically translates to lower borrowing costs for banks, which is then passed on to consumers.

-

Standing Deposit Facility (SDF): Adjusted to 5%.

-

Marginal Standing Facility (MSF) & Bank Rate: Adjusted to 5.50%.

-

Policy Stance: The MPC decided to continue with a "Neutral" stance. This is crucial as it indicates that the RBI is not committed to a unidirectional path; rates could go up or down in the future depending on incoming data, though the current trend is clearly dovish.

-

GDP Projections: The RBI raised its real GDP growth projection for 2025-26 to 7.3%, up from the earlier forecast of 6.8%.

-

Inflation Forecast: The CPI inflation projection for 2025-26 was lowered significantly to 2%, down from the previous 2.6%.

Impact on Your Wallet: Loans and Savings

The most immediate question for millions of Indians is: How does this affect my monthly budget?

1. Home Loans and EMIs

This rate cut is excellent news for borrowers. With the repo rate down to 5.25%, banks and financial institutions are expected to lower their lending rates.

-

Floating Rate Loans: Borrowers with loans linked to external benchmarks (like the repo rate) will see the fastest transmission.

-

The Math: For a home loan of ₹50 lakh with a tenure of 20 years, a 25 bps reduction can reduce the EMI by approximately ₹750 to ₹800 per month. Over the life of the loan, this translates to interest savings of nearly ₹2 lakh.

-

Cumulative Effect: Since the RBI has cut rates by 125 bps throughout 2025, a borrower who took a loan in January 2025 could now see their effective interest rate drop significantly, potentially saving thousands in monthly outflows compared to a year ago.

2. Auto and Personal Loans

Similar to home loans, interest rates on auto and personal loans are expected to soften. This makes big-ticket purchases more affordable just as the year ends, potentially fueling a consumption boom in the consumer durables and automotive sectors.

3. Fixed Deposits (FDs) and Savings

For savers, the news is mixed. A cut in the repo rate generally leads to a reduction in deposit rates.

-

Strategy: If you are a conservative investor relying on FDs, now is the time to lock in rates. Banks will likely start slashing FD interest rates in the coming weeks. Booking a long-term FD at current rates could help you secure higher returns before they dip.

-

Senior Citizens: Those dependent on interest income should review their portfolios immediately to capitalize on existing rates before the downward revision fully kicks in.

Sectoral Impact: Real Estate and Automobiles

Real Estate: A Shot in the Arm

The real estate sector, particularly the affordable and mid-segment housing markets, stands to gain the most. C.S. Setty, Chairman of SBI, noted that the move reinforces structural drivers for a “higher-for-longer” growth trajectory.

-

Affordability: Lower interest rates directly improve the eligibility of potential homebuyers.

-

Sentiment: The psychological boost of a "falling rate regime" often brings fence-sitters back into the market. Developers are optimistic that this cut will clear unsold inventory and spur new project launches in FY26.

Automotive Sector: Revving Up

The auto industry, which often relies on financing for sales (especially for passenger vehicles and two-wheelers), will welcome the lower cost of funds. With the economy growing at over 7% and borrowing becoming cheaper, consumer confidence to purchase vehicles is expected to rise.

Stock Market Reaction

The markets gave a thumbs-up to the policy announcement. The BSE Sensex rallied by 447 points immediately following the news.

-

Why? Lower interest rates reduce the cost of capital for companies, boosting their profitability. Additionally, the RBI’s confidence in the economy (raising GDP forecasts) signals a robust earnings environment for India Inc.

-

Sectors to Watch: Banking, Real Estate, Auto, and NBFC stocks are likely to outperform in the near term as they are direct beneficiaries of the rate cut.

Expert Opinions

Industry leaders have hailed the move as timely and prudent.

-

C.S. Setty (SBI Chairman): Termed the policy as a "clear and confident message" that the Indian economy is on a strong footing. He emphasized that the decision buffers the economy against potential global shocks while keeping the door open for future easing.

-

Real Estate Developers: Major players have expressed that this cumulative reduction of 125 bps in 2025 is a game-changer that will significantly reduce the cost of homeownership.

Conclusion: The Road Ahead

The December 2025 monetary policy update is a testament to India's macroeconomic stability. By prioritizing growth while inflation remains historically low, the RBI has successfully navigated the post-pandemic recovery phase.

For the common citizen, the takeaway is clear: Debt is becoming cheaper, and growth is getting stronger. Whether you are looking to buy a home, invest in the market, or simply manage your household budget, the current economic climate offers distinct opportunities.

As we look toward the next policy review in February 2026, the "Goldilocks" phase seems set to continue, potentially making FY26 a landmark year for the Indian economy.

FAQs

Q1: Will my home loan EMI go down immediately?

A: If your loan is linked to an external benchmark like the Repo Rate (RLLR), your EMI should decrease within the next reset cycle, typically within 3 months. MCLR-linked loans may take longer to adjust.

Q2: Is this a good time to book a Fixed Deposit?

A: Yes. With the repo rate cut, banks are expected to lower FD rates soon. Locking in a long-term FD now allows you to enjoy the current higher rates.

Q3: What does a "Neutral Stance" mean?

A: It means the RBI is not committed to only cutting or only hiking rates. They will decide based on future economic data.

Q4: How much has the repo rate been cut in 2025?

A: The RBI has cut the repo rate by a total of 125 basis points (1.25%) across four occasions in 2025.

Q5: What is the current Repo Rate?

A: As of December 5, 2025, the Repo Rate is 5.25%.